Home of Real Estate News

Home of Real Estate News

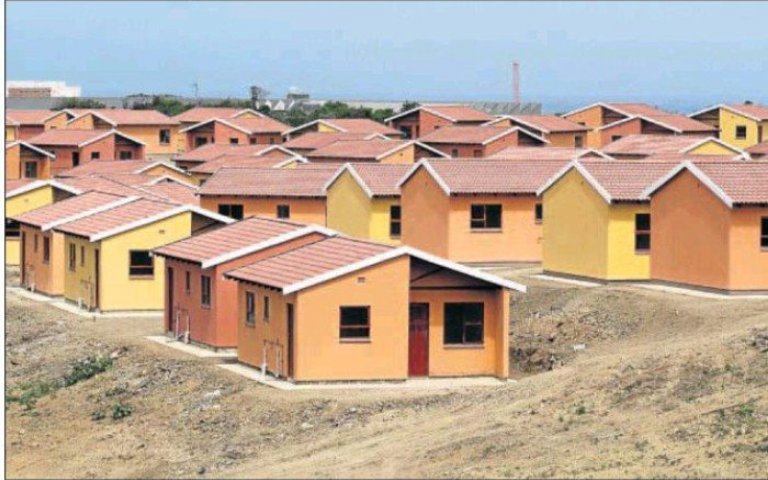

It is estimated that about two-thirds of Kenyan urban households live in informal settlements. This has been caused by rural-urban migration as young people come to urban centres in search of employment. This creates a great need for cheap housing in urban areas thus exerting pressure on housing. It is the desire of each and every individual to own a place to call home. However, the low incomes of many Kenyans prevent them from owning expensive properties offered in the market and they end up considering taking up mortgages. If you have been considering taking up a mortgage below is what you need to know. A mortgage, according to the dictionary, is a legal agreement by which a financial institution lends money at interest in exchange for taking title of the debtor's property. They sum it up with the condition that the conveyance of title becomes void upon the payment of the debt. There are two main types of mortgages in Kenya namely;

While a section of Kenyans desire to take up mortgages as a way to home ownership. The main barriers to mortgage issues according to Centre for Affordable Housing Finance 2019 report is asset-liability mismatch by tenor due to the relatively long term nature of mortgage loans and short-term nature of bank deposits, limited capital markets funding for mortgage resulting in low supply of long- term capital, a complex legal and regulatory framework and collateral requirements making mortgages exceedingly expensive. All these factors have led to low mortgage uptakes in the country. In conclusion, the hope of Kenyans getting cheap mortgages. The Kenya Mortgage Refinancing Company is set to avail mortgages at 7 percent interest for Kenyans earning below Ksh. 150,000. While this will favour a section of Kenyans, the low income earners can consider purchasing affordable land for sale in satellite towns and building their homes gradually and ultimately settle their families.

It is estimated that about two-thirds of Kenyan urban households live in informal settlements. This has been caused by rural-urban migration as young people come to urban centres in search of employment. This creates a great need for cheap housing in urban areas thus exerting pressure on housing. It is the desire of each and every individual to own a place to call home. However, the low incomes of many Kenyans prevent them from owning expensive properties offered in the market and they end up considering taking up mortgages. If you have been considering taking up a mortgage below is what you need to know. A mortgage, according to the dictionary, is a legal agreement by which a financial institution lends money at interest in exchange for taking title of the debtor's property. They sum it up with the condition that the conveyance of title becomes void upon the payment of the debt. There are two main types of mortgages in Kenya namely;

While a section of Kenyans desire to take up mortgages as a way to home ownership. The main barriers to mortgage issues according to Centre for Affordable Housing Finance 2019 report is asset-liability mismatch by tenor due to the relatively long term nature of mortgage loans and short-term nature of bank deposits, limited capital markets funding for mortgage resulting in low supply of long- term capital, a complex legal and regulatory framework and collateral requirements making mortgages exceedingly expensive. All these factors have led to low mortgage uptakes in the country. In conclusion, the hope of Kenyans getting cheap mortgages. The Kenya Mortgage Refinancing Company is set to avail mortgages at 7 percent interest for Kenyans earning below Ksh. 150,000. While this will favour a section of Kenyans, the low income earners can consider purchasing affordable land for sale in satellite towns and building their homes gradually and ultimately settle their families.

Real Estate Kenya News is the leading online real estate news, tips, trends and information website in Kenya. This blog covers diverse topics ranging from housing, mortgages, land, finance and other real estate related topics. Whether you are buying, selling land or houses or you are looking to improve your home, we are here to help you through it all. Do you have a general enquiry, suggestion or something you would like to share with us? We appreciate your feedback, the good and the bad.

Three main documents involved in land transfer in Kenya

Three main documents involved in land transfer in Kenya  Real Estate Bubble in Kenya. Are we in Trouble or it's a Non-issue?

Real Estate Bubble in Kenya. Are we in Trouble or it's a Non-issue?